The RIS industry in the U.S. is currently plagued by market saturation and marginal revenue growth. But thanks to new strategies by PACS vendors, the outlook for the RIS sector may be improving.

The 2001 RSNA meeting kicked off a watershed year for PACS and RIS vendors. Each are vying to grab profits by demonstrating the newest way to combine standard PACS technology and a text-based system to create a full-spectrum electronic patient record. With the RIS sector reaching an 80% market saturation level and characterized by a historically low technological innovation curve, it is little wonder that vendors are anxious to try new tactics to improve their sales hit rate.

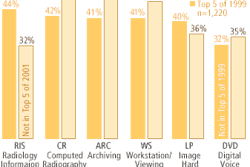

A Frost & Sullivan analysis shows that over 50% of RIS sellers now claim that they have a partnership agreement with "best-of-breed" PACS vendors for co-marketing of their products as combined solutions. This is not unusual, as combined products are discussed as the next wave of radiology information technology.

Participating in a market that has otherwise topped off at around $151 million in annual sales in the U.S., RIS vendors need a shot in the arm to boost sagging sales and produce a solid return for their marketing dollar. Many firms are now hoping to build a commensalist relationship with top-ranking imaging vendors, aiming to piggyback sales using their counterpart's strong market penetration. After all, it might be far more lucrative to garner interest from buyers who are already in the market for a new technology like PACS than to try and win them over with a known commodity.

At this point, it appears that DICOM-HL7 interface brokers will continue to enjoy growing sales, as market demand for RIS/PACS may still be leaning largely toward the connection of disparate systems as opposed to a truly integrated two-in-one solution. Notoriously cost-efficient, hospital buyers are not going to pay extra for a new RIS, even as a component, when they already own a system that works.

Therefore, the new generation of integrated RIS/PACS products may undergo some abrasion from lopsided demand that may ultimately cut into unit sales prices. The estimated $780 million market size (by revenue) for pure PACS products may be somewhat indicative of market size for the integrated RIS/PACS product class over the next few years.

Sales for the RIS market tend to be largely concentrated among the top tier of healthcare information systems vendors, such as Cerner, Meditech, Siemens Medical Solutions Health Services, and Sunquest Information Systems (now a part of Misys Healthcare). Each firm’s large installed base gives it disproportionate leverage among hospitals for replacement sales or software upgrades.

Infiltration by imaging vendors

However, Frost & Sullivan feels that many imaging vendors will begin experimenting with self-made RIS products for sale in conjunction with their PACS offerings. Given the much higher overall leverage that imaging vendors possess with the hospital market, we believe that infiltration from the top tier of this sector will change the market-share picture for RIS products to some degree in the next few years.

Demand momentum seems to still favor stand-alone, department-level RIS purchases. This is expected as U.S. hospitals are gearing up to meet the combined budget hurdles of the Health Insurance Portability and Accountability Act (HIPAA) in the short term and the Medicare crunch in the long term. The great bulk of hospital administrations simply cannot afford anything more than perhaps $600,000 for a departmental system.

Very few hospitals will be in the financial position to opt for enterprise configurations or even integrated RIS/PACS networks in the future. This small sales pool is sure to keep things tight for vendors trying to ward off competition while still maximizing per-unit profit margins.

One of the biggest and riskiest market trends is the application service provider (ASP) movement for integrated RIS/PACS, which is being spearheaded largely by IT vendors hoping to cash in on a wave of enthusiasm for Internet-based deployment over the next few years.

While we certainly feel that the technology is ready for the challenge and that demand will blossom for this deployment model, the staggering cost of infrastructure investment may not be realized in the expected time frame. As a result, many vendors trying to cross over to an ASP model may experience a deflating financial picture.

On the surface, the ASP model would seem to be a good match for this market. While demand for client-server architecture is still generally strong among all HIS products, the nature of image transmission places a heavy burden on storage space. As a result, a high-bandwidth line equipped with an ASP-based deployment mode for image storage, retrieval, and archiving would seem to be a good fit.

However, security concerns persist, complicated further by the mingling of RIS or PACS data into an electronic patient record (as is the push with many new product releases). Therefore, many facilities are electing to wait for the final word from the U.S. Department of Health and Human Services over these deployment issues.

With market growth nearing zero percent, the subsistence economy of RIS may well benefit by the development of a new radiology product such as RIS/PACS -- one that will not supplant RIS, but will be beneficial to its continued existence. We predict an improvement over 2001 RIS sales by about 3% over the short term (the next three years), which we feel is largely attributable to interest in combination purchases among premium, high-budget hospital clients.

Overall, the 2001 RSNA meeting seemed to bring some sparkle back for RIS product development managers and business strategists in the healthcare IS arena. And it's important not to underestimate the relatively high value of radiology products to the entire market for hospital clinical IS products.

With a little marketing grease, Frost & Sullivan believes that RIS/PACS can be a juggernaut combination for sales in the long term, and may become a vital part of the revenue lineup for top-tier and second-tier vendors alike.

By Amith Viswanathan

AuntMinnie.com contributing writer

February, 18, 2002

Mr. Viswanathan is a senior industry analyst with the Healthcare Information Systems Group of Frost & Sullivan, a San Jose, CA-based market consulting and training firm. The information in this article is included in a recently published Frost & Sullivan report on the RIS market. For more information, visit healthcare.frost.com.

Related Reading

Report: PACS to revive RIS market, January 8, 2002

PACS users still waiting for Internet revolution, December 20, 2001

Stop me if you’ve heard this one about PACS, November 29, 2001

Report: U.S. PACS market to hit $1.1 billion by 2010, October 19, 2001

Copyright © 2002 AuntMinnie.com